What Is Credit Control? + 4 Tips To Tighten Credit Control Measures

What Is Credit Control?

Credit control refers to the strategy a business creates when it chooses to issue credit to customers. The strategy addresses important details like credit standards, credit period, and payment terms to promote timely payments.

Offering credit to customers comes with the inherent risk of missed payments, but the benefits are so great that they usually outweigh the risks.

Controlling those risks is important for the health of your business — to keep payments rolling in and customers returning. So, let’s dive in to see how you can make credit control work for your business.

How Credit Control Processes Work

Credit control refers to the protective measures a business takes to make its credit lending procedures more reliable. For your credit control system to work, you’ll want to execute the following:

- Verify customer information: Ensure you have accurate and up-to-date contact information for the customer. This can prevent invoices from being sent to dead inboxes or old addresses, and keep payments on schedule.

- Establish background check procedures: Vetting customers before extending credit is crucial to upholding a credit standard. Decide what sources you’ll use for credit checks, what information you’ll need from their bank, and what will be considered a trustworthy reference.

- Set credit limits: Regardless of your customers’ creditworthiness, your business will only be able to extend a limited amount of credit at a time without it negatively impacting cash flow. Decide what this amount should be and how you’ll go about issuing lines of credit to customers.

- Conduct periodic reviews: The need for credit control is ongoing. Reviewing customer accounts is an important step to figure out what’s working and what’s not. You can use this information to adjust credit limits or change processes to improve results.

These four processes work hand in hand to deliver effective credit control.

Is Credit Control Different From Credit Management?

Credit control means a business is taking steps to offer credit to customers who can honor the terms and conditions of the sale. Credit management, on the other hand, is what follows — when the business actively monitors customer relationships to ensure timely payments.

So, credit control can be understood as setting the stage for efficient credit management.

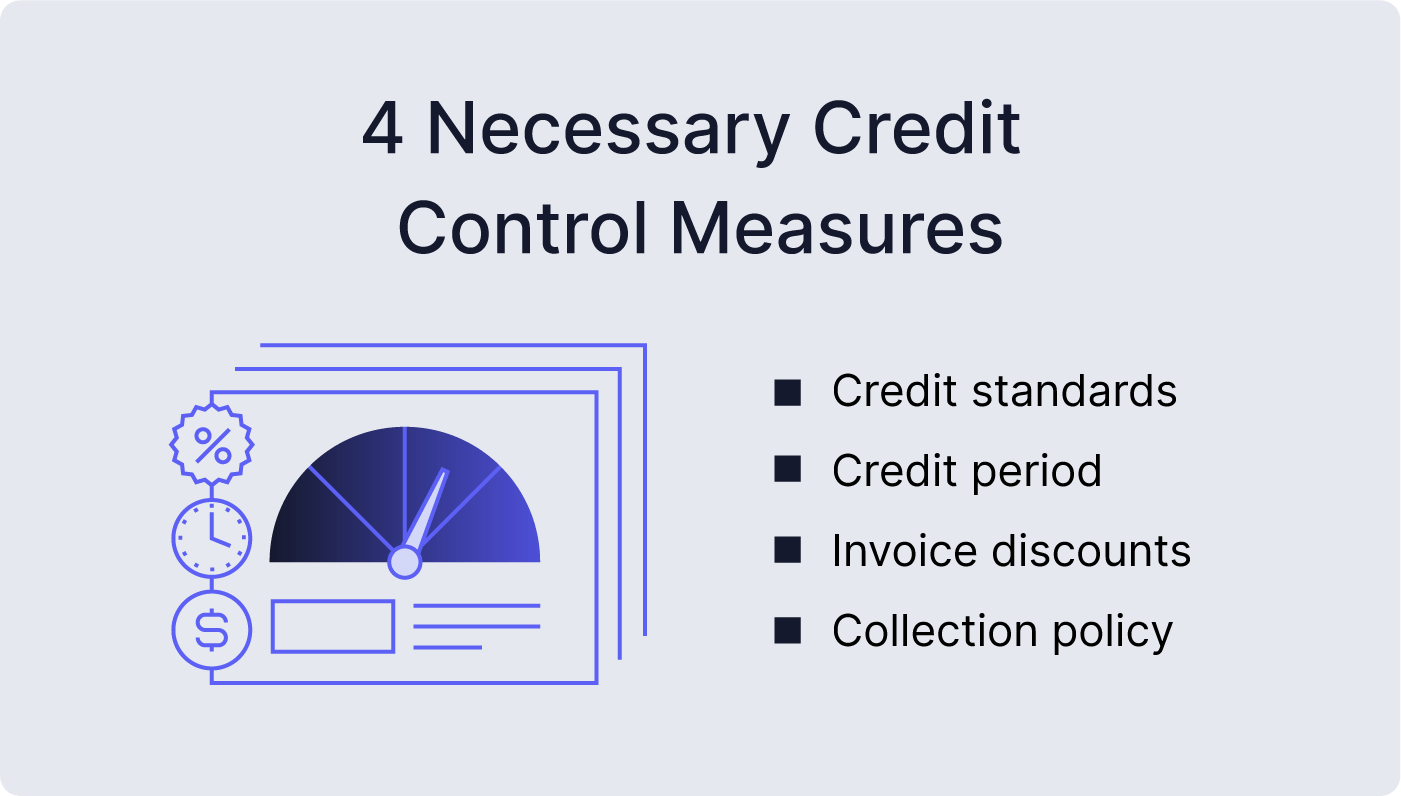

Must-Have Credit Control Measures

There are four primary credit control measures you should pay special attention to:

- Credit standards: Determining a customer’s creditworthiness at the start sets the tone for all other credit control measures. How will you assess a customer’s credit score and credit history?

- Credit period: Offering long credit periods is beneficial to customers, but can interrupt your cash flow. How long can your company afford to go with an outstanding invoice before it interrupts operations?

- Invoice discounts: Offering discounts for early payments can have a positive impact on cash flow. How large a discount can your company afford to offer without negatively impacting profits?

- Collection policy: This factor addresses how lenient or aggressive your company will be in pursuing accounts that are in default. How quickly will you send overdue invoices to collections? When will it be necessary to take legal action?

Identify how your team should go about addressing these measures with customer accounts to improve team effectiveness.

Establishing Credit Control Procedures

Credit control should not be a vague term that’s used lightly. Collect your credit control procedures into an official document that your team can reference and put into action.

Keeping your finance and sales teams aligned on company initiatives is necessary for its overall success. This also requires keeping the document up to date with the findings from your periodic reviews.

Credit Control Policies

When you establish your credit control policy, you’ll also need to decide on the acceptable level of risk you’re willing to expose your business to. This is commonly separated into three categories:

- Restrictive: These policies contain the lowest degree of risk. Consider taking a restrictive approach if you operate with low cash flow or don’t want to leave things to chance with new customers.

- Moderate: These policies seek a balance in protecting the company while still offering customers competitive credit terms.

- Liberal: These policies expose a company to the greatest degree of risk. They are usually implemented by companies that are trying to gain a greater degree of market share.

A business doesn’t need to stay committed to just one credit control approach. For instance, when a company first launches a credit policy, they may adopt a restrictive approach. If their credit initiatives are successful and the economy is strong, then they can turn to a more liberal approach, tightening measures when appropriate.

Credit Control Policies

When you establish your credit control policy, you’ll also need to decide on the acceptable level of risk you’re willing to expose your business to. This is commonly separated into three categories:

- Restrictive: These policies contain the lowest degree of risk. Consider taking a restrictive approach if you operate with low cash flow or don’t want to leave things to chance with new customers.

- Moderate: These policies seek a balance in protecting the company while still offering customers competitive credit terms.

- Liberal: These policies expose a company to the greatest degree of risk. They are usually implemented by companies that are trying to gain a greater degree of market share.

A business doesn’t need to stay committed to just one credit control approach. For instance, when a company first launches a credit policy, they may adopt a restrictive approach. If their credit initiatives are successful and the economy is strong, then they can turn to a more liberal approach, tightening measures when appropriate.

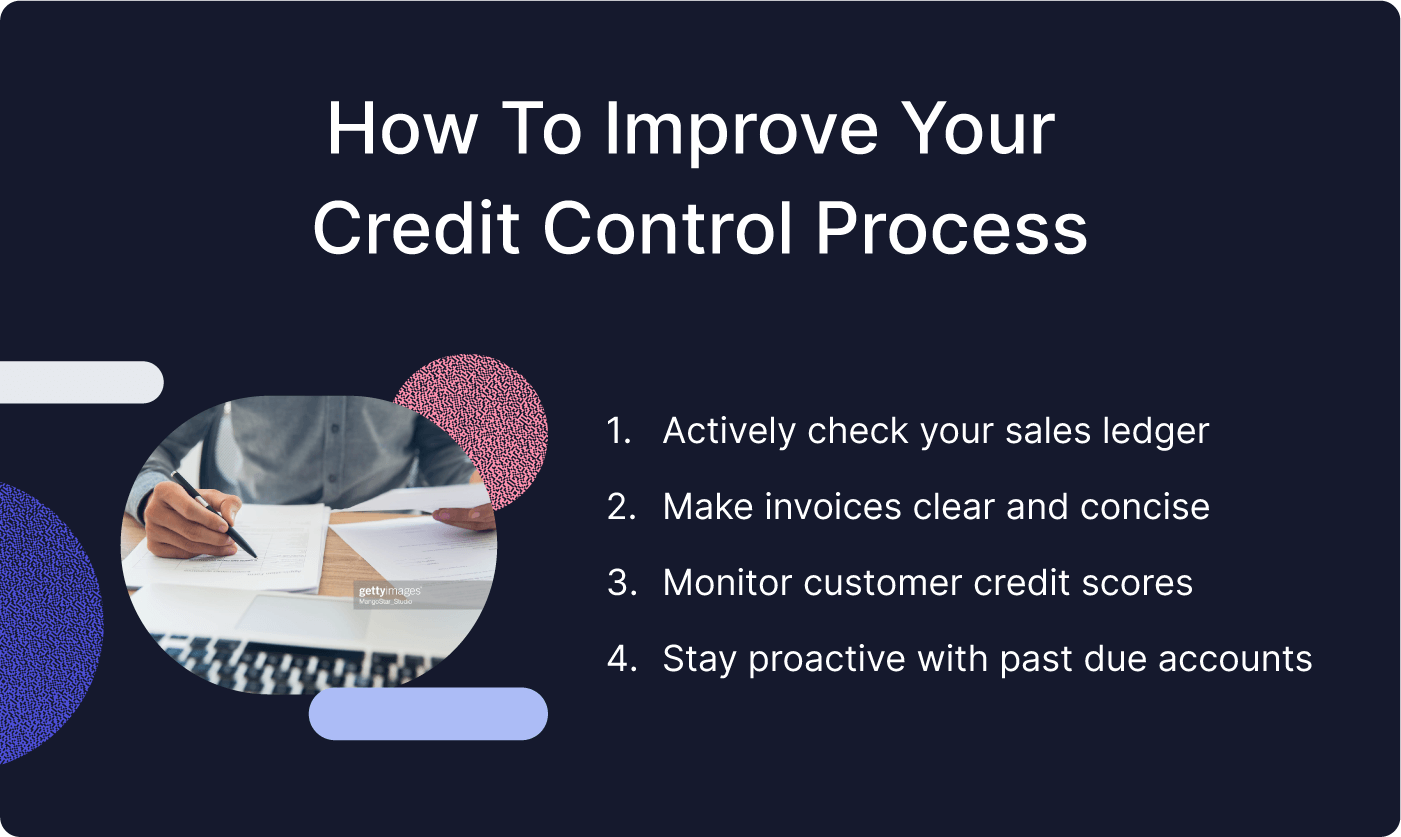

4 Ways To Improve the Credit Control Process

If you already have credit control measures in place but are receiving lackluster results, adopting these practices might turn things around.

- Actively check your sales ledger: Reviewing your ledger regularly will help you catch problems early, potentially preventing them from turning more severe. When you do this, look for how much credit’s been issued, the scheduled payments that are coming up, and deadlines that have passed.

- Streamline invoices: Oftentimes, missed payments are the result of a misunderstanding by the customer of what was required. Rewriting invoices to be clear and concise is one way to minimize this risk. Restate the credit terms and payment methods the customer agreed to uphold so that they have an easy point of reference.

- Monitor customer credit scores: Rerunning credit checks after you’ve entered into a working relationship with a customer is crucial for effective credit management. This can be time-consuming to perform manually, but services like Nuvo can help automate this recurring process.

- Stay proactive: Keep unpaid debts from mounting up by creating an effective dunning process. The longer an invoice goes unpaid, the less likely it is to ever be paid. Follow up quickly and regularly to improve your chances of success and avoid having to involve an outside collection agency.

Now that you have an answer for what credit control is, you’re in a good position to implement it in your own company’s practices. Nuvo can help with executing this important process and more.

What Is Credit Control? FAQ

Look to this additional information for help understanding credit control systems.

What Are the Responsibilities of a Credit Controller?

The credit controller is usually responsible for performing customer credit checks, assessing their creditworthiness in accordance with company policies, and communicating with customers to resolve account disputes.

Why Is Credit Control Calling Me?

A credit controller will contact you if an invoice due date has passed but the company has not received payment yet. Even if you have already made the payment, it is recommended that you respond to the company to resolve the discrepancy and keep your account in good standing.

What Are the Benefits of Effective Credit Control Policies?

Effective credit control policies lead to many benefits, like:

- They minimize bad debt since customers will be more likely to honor the payment terms.

- They can improve cash flow by incentivizing customers to pay on time.

- They broaden the pool of eligible customers by making more comprehensive credit terms.

You may also like